How to Calculate Loan EMI Manually vs Using a Calculator

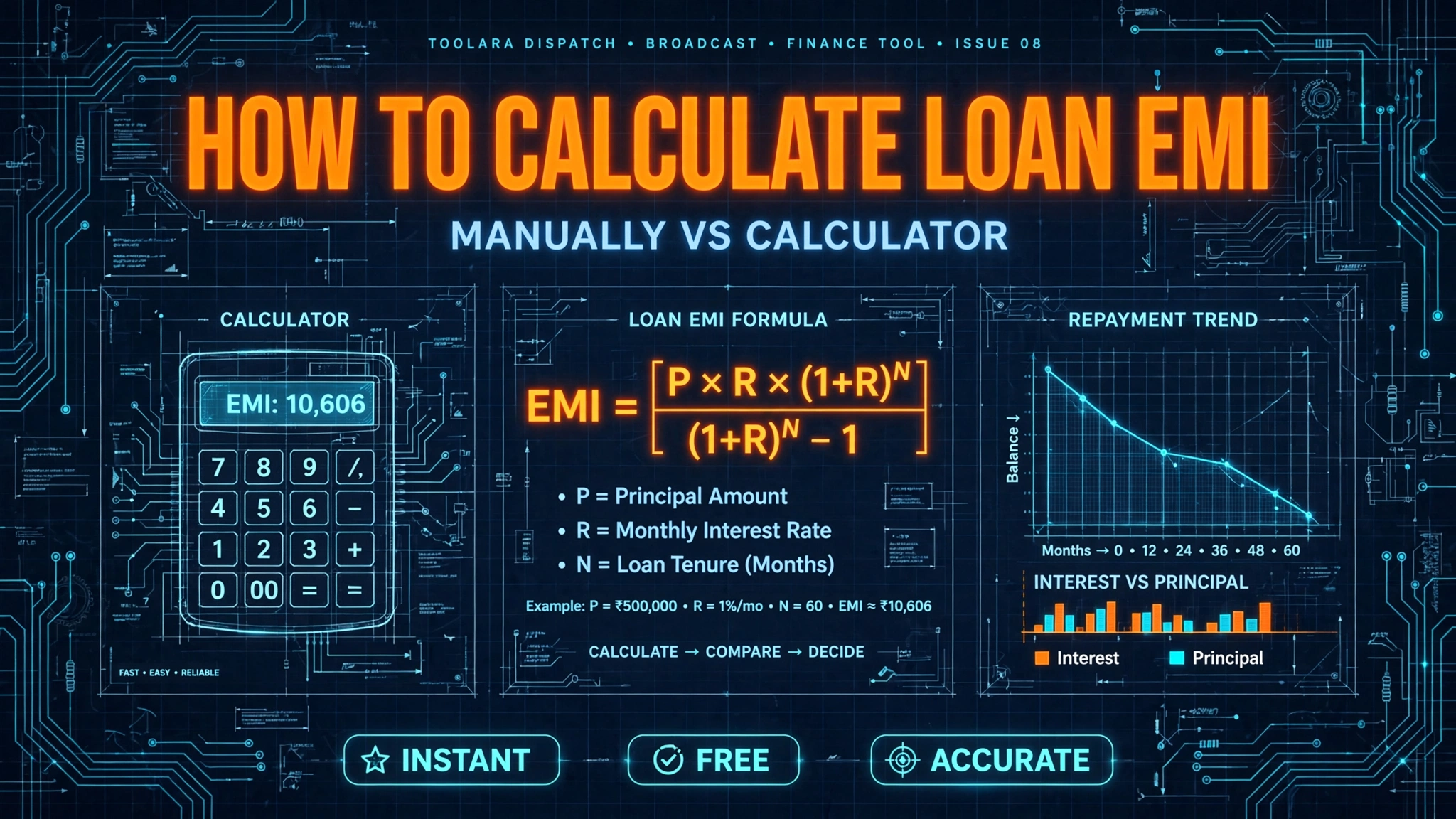

Calculating your loan EMI uses one standard formula: EMI = [P × R × (1+R)^N] / [(1+R)^N – 1], where P is the principal, R is the monthly interest rate, and N is the loan tenure in months. While the math is straightforward, doing it by hand is error-prone — which is why many borrowers use an online EMI calculator for instant, accurate results.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Loan costs vary by lender, product, and jurisdiction. Always consult your lender or a qualified financial adviser before making borrowing decisions.

In this guide, you'll learn exactly how to calculate loan EMI manually with a real example, where people commonly slip up, and how a free calculator gives you the same result in under 5 seconds.

What Is EMI and Why Does It Matter?

EMI (Equated Monthly Installment) is the fixed amount you pay your lender every month until your loan is fully repaid. Each EMI consists of two parts:

- Principal repayment — the actual loan amount being paid back

- Interest payment — the cost charged by the lender

In the early months of a loan, a larger portion of your EMI goes toward interest. As the loan progresses, more of each payment goes toward the principal — a concept called amortization.

Understanding EMI matters because:

- It tells you whether a loan fits your monthly budget

- It helps you compare offers from different lenders

- It reveals the total interest cost over the loan's lifetime

- It empowers you to negotiate better tenure or rates before signing

Whether you're planning a home loan, car loan, personal loan, or education loan, the EMI calculation method is identical when the reducing balance method is used.

The EMI Formula Explained (With Variables Breakdown)

The standard EMI formula used by many banks and lenders is:

EMI = [P × R × (1+R)^N] / [(1+R)^N – 1]

Here's what each variable means:

- P (Principal) — The loan amount you borrow (e.g., $50,000)

- R (Rate of Interest per month) — Annual interest rate ÷ 12 ÷ 100. So if your lender quotes 12% per year, R = 12 / 12 / 100 = 0.01

- N (Number of months) — Loan tenure in months. A 5-year loan = 60 months

- ^ — Exponent operator (raised to the power of)

Important: The interest rate must always be converted to a monthly decimal before plugging it into the formula. This is the most common source of errors in manual calculation.

How to Calculate Loan EMI Manually — Step-by-Step Example

Let's calculate the EMI for a real-world scenario:

Loan amount (P): $100,000

Annual interest rate: 9%

Tenure (N): 5 years = 60 months

Step 1: Convert the interest rate to a monthly decimal

R = 9 / 12 / 100 = 0.0075

Step 2: Calculate (1 + R)^N

(1 + 0.0075)^60 = (1.0075)^60

Using a scientific calculator:

(1.0075)^60 ≈ 1.5657

Step 3: Plug values into the EMI formula

EMI = [100,000 × 0.0075 × 1.5657] / [1.5657 – 1]

EMI = [750 × 1.5657] / 0.5657

EMI = 1,174.28 / 0.5657

EMI ≈ $2,076.04 per month

Step 4: Calculate total payment and interest

- Total payment over 60 months = 2,076.04 × 60 = $124,562.40

- Total interest paid = 124,562.40 – 100,000 = $24,562.40

That's the complete manual breakdown. Notice how a single decimal slip in Step 1 or Step 2 would throw the entire result off by hundreds of dollars.

Manual Calculation Pitfalls: Where People Go Wrong

Even confident math users make these common mistakes:

1. Forgetting to convert annual rate to monthly

Plugging 9 (or even 0.09) directly into R instead of 0.0075 is a frequent error — and it produces a drastically incorrect EMI figure.

2. Mismatching units for tenure

Using years (5) instead of months (60) for N completely breaks the calculation.

3. Rounding too early

Rounding (1.0075)^60 to 1.57 instead of 1.5657 changes the EMI by several dollars per month — and potentially a meaningful amount over the full loan term.

4. Wrong exponent calculation

Without a scientific calculator, computing (1.0075)^60 by hand is difficult to do accurately.

5. Forgetting processing fees and taxes

The formula gives you the pure principal-and-interest EMI, but lenders may also add processing fees, insurance, or applicable taxes that affect your actual total outflow.

Skip the math — use a free EMI calculator

Instead of risking errors that could affect real financial decisions, use the Toolora EMI Calculator. Just enter your loan amount, interest rate, and tenure — and get instant results plus a complete amortization schedule showing how each month's payment splits between principal and interest.

It's free, requires no signup, and applies the same formula shown above.

How to Calculate Loan EMI Using an Online Calculator

Here's how a typical loan EMI calculator works:

- Enter the loan amount (e.g., 100,000)

- Enter the annual interest rate (e.g., 9)

- Enter the loan tenure in years or months (e.g., 5 years)

- Click Calculate

You instantly get:

- Monthly EMI

- Total interest payable

- Total amount payable (principal + interest)

- A month-by-month amortization table

- Often a visual pie chart showing principal vs interest split

Many calculators also let you adjust variables in real time using sliders — so you can see how a rate change or tenure extension affects your monthly payment.

Manual vs Calculator: Side-by-Side Comparison

| Factor | Manual Calculation | Online Calculator |

|---|---|---|

| Time required | 5–10 minutes | Under 5 seconds |

| Accuracy | Prone to rounding/decimal errors | Highly accurate |

| Tools needed | Scientific calculator | Just a browser |

| Amortization schedule | Requires 60+ separate calculations | Generated instantly |

| Comparing multiple scenarios | Tedious — redo entire calc | Adjust slider, see results live |

| Understanding the math | Excellent — you learn the formula | Limited unless explained |

| Best for | Learning, one-off checks | Real loan decisions, comparisons |

Verdict: Use the manual method to understand how EMI works. Then use an online calculator for actual decisions — it's faster, less error-prone, and lets you compare scenarios side by side.

Tips to Lower Your EMI Before You Sign

If your calculated EMI feels too steep, consider these strategies — and discuss them with your lender or financial adviser to understand what's appropriate for your situation:

1. Increase the down payment

A larger down payment reduces P, which directly reduces EMI. Paying more upfront can also reduce total interest paid over the loan term.

2. Extend the tenure (carefully)

A longer N means smaller EMI — but you'll pay more total interest. Use a calculator to find the right balance for your circumstances.

3. Negotiate the interest rate

Even a small rate reduction can make a meaningful difference over a long loan term. A strong credit history and existing relationship with the lender may help.

4. Understand reducing balance vs flat rate

Reducing balance interest calculations differ from flat rate calculations. Ask your lender which method they use, as this affects the true cost of the loan.

5. Make prepayments when possible

Lump-sum prepayments toward principal reduce your outstanding balance. Check whether your lender charges a prepayment penalty before doing so.

6. Compare lenders

Running the same loan scenario through multiple lenders can help you identify more competitive offers. Always compare the annual percentage rate (APR) or equivalent total cost figure, not just the headline interest rate.

7. Watch out for additional fees

Processing fees, prepayment penalties, and bundled insurance can increase your effective borrowing cost. Always ask for a full breakdown of the total cost of credit.

Frequently Asked Questions About EMI Calculation

1. Can I calculate EMI without using the formula?

Yes — an online EMI calculator does the math for you instantly. You just enter the loan amount, rate, and tenure. Understanding the formula is useful, but not required for everyday use.

2. Does the EMI formula work for all loan types?

The formula applies to loans where the lender uses the reducing balance method, which is common for home loans, car loans, personal loans, and education loans. Always confirm the interest calculation method with your lender, as some products use different approaches.

3. Why does my actual EMI differ slightly from my calculation?

Lenders may add processing fees, applicable taxes, or insurance premiums on top of the base EMI. They may also apply slightly different rounding conventions. The standard formula covers principal and interest only.

4. How does increasing the loan tenure affect EMI and total interest?

Longer tenure means a lower monthly EMI but higher total interest paid. For example, a longer-term home loan will typically cost less each month but more overall. The exact difference depends on the loan amount and interest rate — a calculator can help you model specific scenarios.

5. Is there a quick mental shortcut to estimate EMI?

Rough rules of thumb exist (for example, some people estimate monthly EMI as approximately 1% of the loan amount for a 10-year loan at moderate interest rates), but these vary significantly by rate and tenure and should not be relied upon for financial decisions. Use a dedicated calculator for any meaningful estimate.

Calculate Your EMI in Seconds — For Free

Manual calculation is useful for understanding the math, but when real money is on the line, accuracy matters. Try the free Toolora EMI Calculator to instantly compute your monthly EMI, total interest, and full amortization schedule — no signup required.

Compare multiple loan scenarios, adjust the tenure or rate, and go into lender conversations better informed. Calculate your loan EMI now →